Scary season is here and while an accountant costume may not scare many people, here are three lease accounting challenges that will frighten any finance professional.

1. Balance sheets that don’t balance

This horrifying image is enough to send any accountant into a spin. When all the journal entries balance and everything reconciles, yet total assets don’t equal liabilities and equity – what’s happened? Hint: Put an unbalanced balance sheet in your window when you share screen to deter any accountants from bothering you.

2. Hard-coded numbers in an Excel document

Tracing an amount back to its source can be rewarding, but when it turns out that ‘some number’ has been typed in, that’s not from the data source, it will send chills down the spine of an accountant. Accountants like to understand where numbers come from and to explain them all, but formulas with rogue amounts added in make this difficult.

3. A missed deadline

Monthly or annual reporting cycles only run smoothly when each milestone along the way is met and on time. So, when a deadline is missed through a task not being done or a document not sent through on time, accountants will turn inside out.

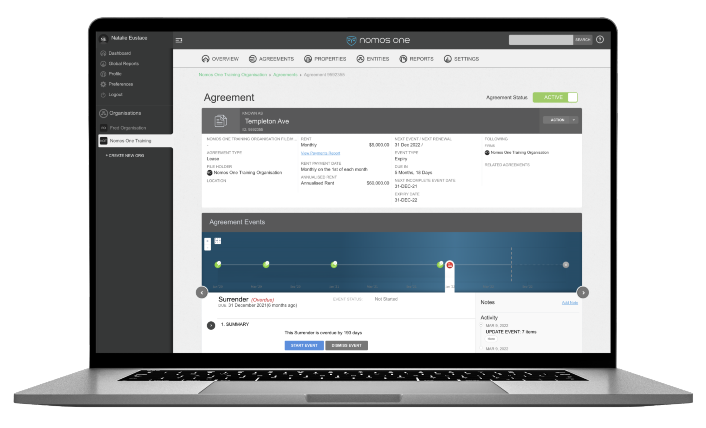

Avoid these terrifying situations (and let the accountants rest easy)

Does your business have leased assets? Do you need to report on these under IFRS 16 (AASB 16)? Nomos One is your lease accounting and lease management solution that can spare your accountants from the horrors of lease accounting challenges. Book a demo today.